Program Trading and Plunge Protection

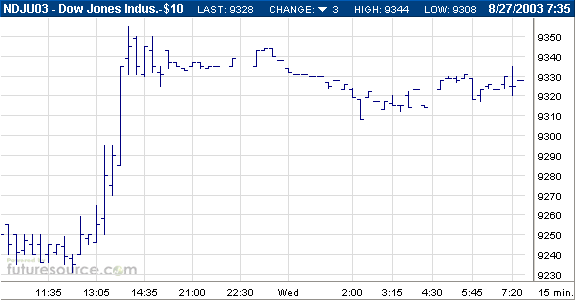

Did some pinch-hitting for the Daily Reckoning this morning and wrote the notes that normally come from Eric Fry. Some of what you see here you may also see in the DR. But the nice thing about publishing here is that I can show you some pictures to go along with the story. So that's what I'll do.... If you're reading this kind of information, odds are that at some point you've heard of the "Plunge Protection Team" or PPT. The PPT, the conspiracy goes, is a the active arm of the President's Working Group on Financial Markets. The Working Group was formed by executive order in 1988 during Ronald Reagan's first term. After the 1987 crash, its goals were to "[enhance] the integrity, efficiency, orderliness, and competitiveness of our Nation's financial markets and [maintain] investor confidence." The order goes on to say that, "To the extent permitted by law and subject to the availability of funds therefore, the Department of the Treasury shall provide the Working Group with such administrative and support services as may be necessary for the performance of its functions." No where in the order does it say the Working Group is responsible for causing stock market rallies late in the day to soothe a jittery public and keep the politicians happy. But I guess you wouldn't expect to find that in the print...even the fine print. Still, the existence of the PPT is one way to explain how you can reverse an entire day of selling on the Dow by buying futures contracts on the big indexes during the last two trading hours of the day. Suddenly, what looks like an 81-point loss and getting worse is a modest 22.81-point gain--and within striking distance of the 14-month high the Dow set last week. More on the PPT below. Maestro Greenspan and his merry men COULD orchestrate a reversal by buying an enormous amount of S&P or Dow futures contracts late in the day. How would it work? The easiest way would be to buy front-month futures contracts on the S&P and increase the spread between the futures market and the cash index. The spread is the difference between the fair value of the cash index and what the futures market is pricing the index at. By buying S&P futures, you increase the "spread" between the futures market and the actual cash index. And if the spread gets big enough, program trading kicks in to buy the cash index rather than the futures. Could you prove this is happening? Well, you could look at prices for front month futures contracts on the Dow and S&P and see what kind of buying took place between, say, 1:00 p.m. and 2:00 p.m. yesterday. If you looked at the front-month DJIA composite here's what you'd find: Dow Futures Rising What does this show you? Well...I'm not a futures expert. And I'm not sure if this necessarilyily the right contract to look at. But it looks to me like a little after 1 p.m., there was a whole lot of buying in the front month Dow futures contract. And what happened to the Dow itself after 1 p.m.? Take a look....

Interestinging, no?

Was this just the market shaking off the bad news and looking on the sunny side of life? Or did the futures buying trigger buying on the cash index?

To answer that, you could check to see what the program trading statistics were for the day in question. The Wall Street Journal publishes program trading stats on a weekly basis. And according to the Journal, in the last four weeks starting on July 25th, program trading has accounted for 38.5%, 42%, 45.5%, and 39.9% of the total trading volume for the NYSE.

The August 22nd Journal reports that for all the program trades on the NYSE during the week ended August 15th, "13.6% involved stock-index arbitrage" and that "Some 53.9% of program trading was executed by firms for their clients."

Is Uncle Sam a client? And is he pumping money to accounts set up with the big brokers on Wall Street to buy futures and cause program trades to kick in and buy the cash index?

I report, you surmise.

Interestinging, no?

Was this just the market shaking off the bad news and looking on the sunny side of life? Or did the futures buying trigger buying on the cash index?

To answer that, you could check to see what the program trading statistics were for the day in question. The Wall Street Journal publishes program trading stats on a weekly basis. And according to the Journal, in the last four weeks starting on July 25th, program trading has accounted for 38.5%, 42%, 45.5%, and 39.9% of the total trading volume for the NYSE.

The August 22nd Journal reports that for all the program trades on the NYSE during the week ended August 15th, "13.6% involved stock-index arbitrage" and that "Some 53.9% of program trading was executed by firms for their clients."

Is Uncle Sam a client? And is he pumping money to accounts set up with the big brokers on Wall Street to buy futures and cause program trades to kick in and buy the cash index?

I report, you surmise.

posted by Daniel @ 8/27/2003 01:53:00 PM

0 comments

![]()

{kind=link}

0 Comments:

Post a Comment

<< Home