Unrestricted Warfare and the Dollar

This post is more like an essay. I'm trying to put a table of contents at the top here so you can quickly scan what's new and jump to what's interesting to you, rather than having to scroll. Be patient with me. (Meditate, if it helps...outside the office right now I hear the chanting of a a Buddhist(?) monk who comes by the window about the same time every night...his voice sounds just like a didgeridoo...amazing.) In the meantime, this is another example of the kind of content--in addition to the investment content--that this medium allows me to publish. It's a more detailed exploration than I could undertake in an e-mail or a monthly issue. And since I'm not actually sending it to you, I assume I'm not imposing. And if you really really think it's too long...stop reading. Otherwise...enjoy. Unrestricted Warfare and Destroying the Dollar “If it wanted to, and if it were smart enough, how could a terrorist organization destroy the U.S. dollar?” This is the question I posed to myself last night over a few beers at my favorite bar, just off rue St. Denis. It wasn’t originally my question. It was posed to me by a reader at the conference in San Francisco. This reader happens to be a Naval Reserve officer. And he and his professional friends do a lot of thinking about what terrorists may or may not be plotting against American interests. “How they might come after the dollar,” he said, “is what keeps the intelligence boys up at night.” The premise of this line of thinking is simple: If you really wanted to cripple the United States, or even send it back to the Middle Ages, you wouldn’t bomb its buildings, bridges, buses, or bourses. You’d destroy its currency. It’s the dollar that gives America its power, the thinking goes. It’s the dollar that makes America strong. It’s the dollar, and the willingness of foreigners to own it via U.S. stocks and bonds that is the source of American strength. It’s the strong dollar that pays for aircraft carrier groups, precision guided missiles, Stryker brigades, and the C-17s that fly American men and weapons to all four corners of the globe. Destroy the dollar, and you destroy America. Practically speaking, there are probably things you COULD to the physical currency to sow chaos in financial markets. You could counterfeit your enemy’s money, like the British did in the Revolutionary War (while they paid their own debts in gold.) Or you could sprinkle anthrax at an ATM in the heart of a major city. That would complicate the use of physical money. Of course there are a lot more digital dollars than real dollars these days. No one knows exactly how many. But the Depository Trust Clearing Corporation clears $1 quadrillion worth of trading activity every year. I’m not even sure what that means, but it amounts to about $3 trillion and 4 billion trades a day. It does all that clearing on computers located at facilities located all over the country. In one of his novels, Tom Clancy had terrorists destroying one of those facilities and vanquishing Wall Street into the ether. Today, they’d have to find them. Then there’s the Federal Reserve, which clears all international trading in dollars. A reader on the message board wrote the following. Although I can’t vouch for its accuracy, it seems plausible: On 9/21/01, I attended a small, private meeting where a senior official of the Fed. Reserve briefed us on the recent calamity in New York. Some of his comments were startling. The New York Fed. Reserve was knocked out by cables that ran under the collapsed buildings. (not reported in the press) The New York Fed is the clearing house for ALL international trading in dollars. The rest of the Fed districts stepped in to share the load and to continue the world trade in dollars. There was a run on the banks in Florida. Little old men and women ran to their bank and demanded all of their assets in cash. The Fed was able to keep this out of the media. In order to stem any further panic, the Fed started injecting 100 billion a day into the system. We were informed that the "normal" cash injection was 1 billion a day. As of our meeting date (9/21/01) they were still injecting at that rate. Our speaker informed us that these funds would be removed from the system when things got back to normal. Then, during a Q/A session that followed his presentation, I asked a "doomsday " scenario question like, "What is your fallback if all your actions are futile?" His response startled me. His words. "We at the Fed will to anything, including direct intervention in capital markets, in order to stabilize the situation." If you really wanted to attack the dollar, you’d attack the electronic clearing systems that make dollar-denominated trade possible. Right? I suppose all of this is possible. But as I was thinking about all this I thought two things. First, the dollar is not really the source of American wealth. A currency doesn’t make a country rich. A sound currency is, perhaps, accompanies a wealthy country. But it’s not the paper that makes you rich. It’s the factories, property, raw materials, labor, knowledge, and skill that are the real source of wealth. Paradoxically, a currency can’t make you strong. In fact, all it can really do is make you weak. Even it’s strength, for America, has been its weakness. The strong dollar has made it possible for Americans to acquire lots of cheap goods and services. But it’s also encouraged a structural shift in the American economy that FAVORS consumption over production. And now, our dollar is our Achilles heel. If foreigners aren’t willing to own it, the dollar will have to depreciate and American standards of living will have to fall. Second, who needs a terrorist to accomplish what the Central Bank is achieving with stunning success. Without a box cutter, and without firing a shot, blowing up a bus, or hijacking an airplane, Greenspan et. al have already done more damage to the dollar than any al Qaeda operative ever could. Who needs an enemy to counterfeit your currency when your own bankers can do it themselves? And all perfectly legally, with the approbation of the public? As an investment question, there’s not much you can do about preventing a theoretical terrorist attack on the dollar. But there IS something you can do about the Fed’s attack. Short bonds. Think of the U.S. government as a company. Its main product is dollars. That product is defective. The proxy for that product is the government bond, which is a call on future dollars, and trades openly in the market. I’ve written a lot about shorting the dollar via bonds this week. So I won’t elaborate here. Nor will I elaborate on the other way to be short the dollar…by being long gold. We’ve spent a lot of time on that too. If you haven’t seen those posts, pay special attention to the chart below showing the ratio between Gold and U.S. T-bonds. This ratio represents, as my trading friend Greg Weldon says, the “Ultimate Battle Between Paper and Gold.” As you can see from the chart, bonds creamed gold for 15 years. That trend is now reversing. Of course you have a risk either way…being short bonds or long gold. The Fed can be the buyer of last resort in the bond market (or encourage the Japanese to buy) and it can be the seller of last resort in gold (although no one can be really sure how much gold is really left in Fort Knox, or if it’s all been leased away to the bullion banks, never to be seen again.) No matter which way you slice it, the real battle in financial markets is not between al Qaeda and the dollar. It’s between paper and gold. And gold is starting to win. But don’t expect paper to go down without a fight.

posted by Daniel @ 8/29/2003 07:11:00 PM

0 comments

![]()

This chart is a long-term chart of gold futures. In his daily Metal Monitor commentary, Greg says, "Of specific, bullish, long-term technical interest, as plotted in the monthly gold chart above, we note:

*Confirmed upside violation of downtrend line in place since 1987

*Massive inverted head-and-shoulders bottoming pattern

*Mega-long-term 36-month Moving Average trending higher

*Moving average at highest level since 1999

"Can anyone say gold at $416? How about $502?"

Three other important things to watch in the gold price, according to Greg. First, if gold closes today above the weekly close of $369.90, it would represent a new bull move WEEKLY closing high. Second, If gold closes August above the monthly close of $368.30 (set in Jan. 03) it would represent a new bull move MONTHLY closing high. And finally, if gold violates the bull move intra-day, intra-week, intra-month high of $384, it would represent a new bull move MULTI-YEAR high.

Notice a pattern here?

And then there's the gold/U.S. T-Bond Ratio. Yesterday I speculated that the big move in uh-hedged gold stocks on the HUI, coupled with the undersubcribed 2-year treasury auction, suggested that dollar disinvestment has begun. If you want a picture that explains it lot more succinctly, look at this...

This chart is a long-term chart of gold futures. In his daily Metal Monitor commentary, Greg says, "Of specific, bullish, long-term technical interest, as plotted in the monthly gold chart above, we note:

*Confirmed upside violation of downtrend line in place since 1987

*Massive inverted head-and-shoulders bottoming pattern

*Mega-long-term 36-month Moving Average trending higher

*Moving average at highest level since 1999

"Can anyone say gold at $416? How about $502?"

Three other important things to watch in the gold price, according to Greg. First, if gold closes today above the weekly close of $369.90, it would represent a new bull move WEEKLY closing high. Second, If gold closes August above the monthly close of $368.30 (set in Jan. 03) it would represent a new bull move MONTHLY closing high. And finally, if gold violates the bull move intra-day, intra-week, intra-month high of $384, it would represent a new bull move MULTI-YEAR high.

Notice a pattern here?

And then there's the gold/U.S. T-Bond Ratio. Yesterday I speculated that the big move in uh-hedged gold stocks on the HUI, coupled with the undersubcribed 2-year treasury auction, suggested that dollar disinvestment has begun. If you want a picture that explains it lot more succinctly, look at this...

Today’s Wall Street Journal reported that “investors have bid emerging-markets bonds to their strongest level in five years.” The article goes on to caution that, “the supply-demand situation could shift against emerging-markets issuers” and that “Emerging-markets nations may soon find themselves in stronger competition to borrow internationally with the U.S. government.”

Competition indeed. The tone of the article seems to suggest that if investors are forced to choose between buying an ever-increasing supply of U.S. debt and emerging market debt, they’ll choose U.S. debt. Well…it HAS been true for the last 10 years.

But as I showed yesterday, the world’s voracious appetite for U.S. debt may be diminishing…primarily because the U.S. government projects nothing but greater and greater deficits for the next 10 years.

It really comes down to whether you believe investors will continue demanding U.S. bonds, no matter how large the deficit gets. Vincent Truglia, co-manager of Moody's Investors Services' sovereign risk unit, said in the Journal article that "A large [budget] deficit, keeping everything else equal, means the U.S. will be the largest drawer upon world savings," making less money available for emerging-market countries, he said.”

Maybe. But only if the world keeps lending its savings to a belligerent American government that’s financing its war machine with the export-driven profits of emerging market countries. And THAT is an issue which deserves a much fuller treatment, which I’ll get to later this afternoon. For now, beware bonds.

Today’s Wall Street Journal reported that “investors have bid emerging-markets bonds to their strongest level in five years.” The article goes on to caution that, “the supply-demand situation could shift against emerging-markets issuers” and that “Emerging-markets nations may soon find themselves in stronger competition to borrow internationally with the U.S. government.”

Competition indeed. The tone of the article seems to suggest that if investors are forced to choose between buying an ever-increasing supply of U.S. debt and emerging market debt, they’ll choose U.S. debt. Well…it HAS been true for the last 10 years.

But as I showed yesterday, the world’s voracious appetite for U.S. debt may be diminishing…primarily because the U.S. government projects nothing but greater and greater deficits for the next 10 years.

It really comes down to whether you believe investors will continue demanding U.S. bonds, no matter how large the deficit gets. Vincent Truglia, co-manager of Moody's Investors Services' sovereign risk unit, said in the Journal article that "A large [budget] deficit, keeping everything else equal, means the U.S. will be the largest drawer upon world savings," making less money available for emerging-market countries, he said.”

Maybe. But only if the world keeps lending its savings to a belligerent American government that’s financing its war machine with the export-driven profits of emerging market countries. And THAT is an issue which deserves a much fuller treatment, which I’ll get to later this afternoon. For now, beware bonds.

The chart shows the Oil Service Holders (OIH) and Halliburton taking off at 10:30, while the Amex Oil Index of integrated majors (XOI) and Exxon logged more modest gains. OIH finished the day up 3.16% and HAL finished up 3.89%

There was no major economic news to explain why the service stocks outperformed the majors. There was this bit, though, from CBS.marketwatch.com, which, by the way, reinforces the idea that buying futures on any index or asset (the Dow, S&P, gold, or oil), can influence the cash index.

“Oil service stocks rallied smartly in midday trading Thursday,

boosted by strength in energy futures…In commodities trading

on the New York Mercantile Exchange, October crude rose 32

32 cents to $31.53 a barrel…”

In fact, every single one of the 18 stocks in OIH was up yesterday. Of course, it’s not realistic that you would have bought EVERY single one of them. That’s really the point though, isn’t it?

With vehicles like OIH, you don’t HAVE to buy every single one and take 18 different risks. You have one risk. And that one risk is leveraged to benefit if you’re right about your idea.

MARKET IMPLICATION: 61 IS A KEY LEVEL FOR OIH. IF IT CAN BREAK OUT OF THAT, IT’S CLEAR TECHNICAL SAILING UP TO ABOUT TO ABOUT 70, THE LEVEL IT LAST SAW IN MAY OF LAST YEAR.

The chart shows the Oil Service Holders (OIH) and Halliburton taking off at 10:30, while the Amex Oil Index of integrated majors (XOI) and Exxon logged more modest gains. OIH finished the day up 3.16% and HAL finished up 3.89%

There was no major economic news to explain why the service stocks outperformed the majors. There was this bit, though, from CBS.marketwatch.com, which, by the way, reinforces the idea that buying futures on any index or asset (the Dow, S&P, gold, or oil), can influence the cash index.

“Oil service stocks rallied smartly in midday trading Thursday,

boosted by strength in energy futures…In commodities trading

on the New York Mercantile Exchange, October crude rose 32

32 cents to $31.53 a barrel…”

In fact, every single one of the 18 stocks in OIH was up yesterday. Of course, it’s not realistic that you would have bought EVERY single one of them. That’s really the point though, isn’t it?

With vehicles like OIH, you don’t HAVE to buy every single one and take 18 different risks. You have one risk. And that one risk is leveraged to benefit if you’re right about your idea.

MARKET IMPLICATION: 61 IS A KEY LEVEL FOR OIH. IF IT CAN BREAK OUT OF THAT, IT’S CLEAR TECHNICAL SAILING UP TO ABOUT TO ABOUT 70, THE LEVEL IT LAST SAW IN MAY OF LAST YEAR.

PLUS

PLUS  The best of both cultures. The only mistake I made was telling Francoise, who sits next to me here in the office. She looked at me somewhat shocked and said, "The poor

The best of both cultures. The only mistake I made was telling Francoise, who sits next to me here in the office. She looked at me somewhat shocked and said, "The poor  The HUI is just now reaching the levels it was at when the tech boom started--when investors had written off gold for dead. Gold, however, has risen from its 6-year grave on the HUI. It has begun.

The HUI is just now reaching the levels it was at when the tech boom started--when investors had written off gold for dead. Gold, however, has risen from its 6-year grave on the HUI. It has begun.

MARKET IMPLICATION: It’s a speculator’s market right now. Look for in-the-money puts on indexes that are overextended. And on the long side, look for calls on gold, gold indexes, and gold stocks.

In particular, look below for OIH, the oil service holder, to break out above 61 on both escalating geopolitical tensions and the new contract awarded to Halliburton for rebuilding Iraqi oil infrastructure. Even HAL calls don’t look like such a bad idea. But why take the risk on HAL when you can own it as part of OIH and get the rest of the sector too?

MARKET IMPLICATION: It’s a speculator’s market right now. Look for in-the-money puts on indexes that are overextended. And on the long side, look for calls on gold, gold indexes, and gold stocks.

In particular, look below for OIH, the oil service holder, to break out above 61 on both escalating geopolitical tensions and the new contract awarded to Halliburton for rebuilding Iraqi oil infrastructure. Even HAL calls don’t look like such a bad idea. But why take the risk on HAL when you can own it as part of OIH and get the rest of the sector too?

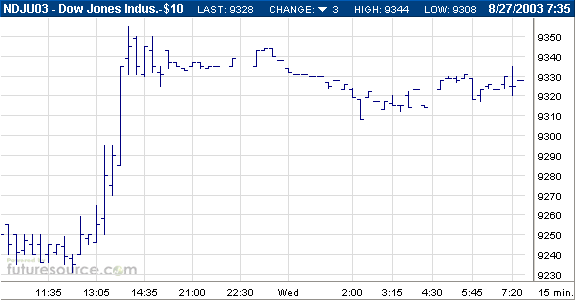

Obviously, bond prices are falling. I WAS looking for a rally. But once real dollar disinvestment begins, there's no telling how far prices could fall, or how high yields could rise.

What about the dollar?

The dollar is up to about $1.08 against the euro in early trading this morning in London. U.S. GDP numbers come out today. And the market expects them to be better than previous estimates. This is just how the bulls envision it: superior economic growth in the U.S. supports the dollar and the stock market. And it's true, the dollar is up about 9% from its May 27 low of $1.19 against the euro.

Yet two obvious facts are ignored in the press reports. First, a stronger dollar makes the current account deficit worse. It makes American goods more expensive...and cuts any expansion off at the knees. Over time, this is bad for the dollar, not good.

Second, and more importantly, it would take a much higher level of economic growth to escape the drag of a growing Federal deficit.

What we have here is a giant game of risk assessment. I'll write more on this later today. If you choose to own dollars now (buy U.S. bonds or stocks), you're betting that higher U.S. growth will make the dollar more appealing than the euro, the yen, or gold.

But your risk is that the growth isn't real economic growth. Your risk is that today's higher GDP numbers are caused by the tax cuts and government spending. Will this "stimulus" be enough to actually create new economic growth, to pare the unemployment roles, to reverse the outsourcing of blue and white collar jobs, and erase the $32 trillion in aggreage U.S. debt? I think not.

IMMEDIATE INVESTMENT IMPLICATION: LOOK FOR FALLING BOND PRICES TODAY, A MODEST RISE IN STOCKS, BUT WEAKNESS IN THE DOLLAR AND STRENGTH IN GOLD. TRADERS COULD BUY PUTS ON TLT AND IEF.

Obviously, bond prices are falling. I WAS looking for a rally. But once real dollar disinvestment begins, there's no telling how far prices could fall, or how high yields could rise.

What about the dollar?

The dollar is up to about $1.08 against the euro in early trading this morning in London. U.S. GDP numbers come out today. And the market expects them to be better than previous estimates. This is just how the bulls envision it: superior economic growth in the U.S. supports the dollar and the stock market. And it's true, the dollar is up about 9% from its May 27 low of $1.19 against the euro.

Yet two obvious facts are ignored in the press reports. First, a stronger dollar makes the current account deficit worse. It makes American goods more expensive...and cuts any expansion off at the knees. Over time, this is bad for the dollar, not good.

Second, and more importantly, it would take a much higher level of economic growth to escape the drag of a growing Federal deficit.

What we have here is a giant game of risk assessment. I'll write more on this later today. If you choose to own dollars now (buy U.S. bonds or stocks), you're betting that higher U.S. growth will make the dollar more appealing than the euro, the yen, or gold.

But your risk is that the growth isn't real economic growth. Your risk is that today's higher GDP numbers are caused by the tax cuts and government spending. Will this "stimulus" be enough to actually create new economic growth, to pare the unemployment roles, to reverse the outsourcing of blue and white collar jobs, and erase the $32 trillion in aggreage U.S. debt? I think not.

IMMEDIATE INVESTMENT IMPLICATION: LOOK FOR FALLING BOND PRICES TODAY, A MODEST RISE IN STOCKS, BUT WEAKNESS IN THE DOLLAR AND STRENGTH IN GOLD. TRADERS COULD BUY PUTS ON TLT AND IEF.

Interestinging, no?

Was this just the market shaking off the bad news and looking on the sunny side of life? Or did the futures buying trigger buying on the cash index?

To answer that, you could check to see what the program trading statistics were for the day in question. The Wall Street Journal publishes program trading stats on a weekly basis. And according to the Journal, in the last four weeks starting on July 25th, program trading has accounted for 38.5%, 42%, 45.5%, and 39.9% of the total trading volume for the NYSE.

The August 22nd Journal reports that for all the program trades on the NYSE during the week ended August 15th, "13.6% involved stock-index arbitrage" and that "Some 53.9% of program trading was executed by firms for their clients."

Is Uncle Sam a client? And is he pumping money to accounts set up with the big brokers on Wall Street to buy futures and cause program trades to kick in and buy the cash index?

I report, you surmise.

Interestinging, no?

Was this just the market shaking off the bad news and looking on the sunny side of life? Or did the futures buying trigger buying on the cash index?

To answer that, you could check to see what the program trading statistics were for the day in question. The Wall Street Journal publishes program trading stats on a weekly basis. And according to the Journal, in the last four weeks starting on July 25th, program trading has accounted for 38.5%, 42%, 45.5%, and 39.9% of the total trading volume for the NYSE.

The August 22nd Journal reports that for all the program trades on the NYSE during the week ended August 15th, "13.6% involved stock-index arbitrage" and that "Some 53.9% of program trading was executed by firms for their clients."

Is Uncle Sam a client? And is he pumping money to accounts set up with the big brokers on Wall Street to buy futures and cause program trades to kick in and buy the cash index?

I report, you surmise.

And here's a Styker unloading in close-quarters from a C-130, courtesy of the Air Force:

And here's a Styker unloading in close-quarters from a C-130, courtesy of the Air Force:

By the way, if you want to reach an interesting account of Russian operations in Chechnya, which depended heavily on the use of wheeled personnel carriers with similar armaments like the Strykers', look at this Rand Corporation report: http://www.rand.org/publications/CF/CF162/CF162.appb.pdf . It contains some amazing details about Russian operational planning for the Russian's first invasion of Chechyna, including one where an entire Russian column was blocked from getting to Chechyna by a local automarket in Russia where some 8,000 people gathered regularly on Saturday's to buy and sell cars.

It's not really a laughing matter, of course. Presuambly, the Army knows the dangers of using even fast moving armored columns in hostile areas. For one they've just had a lot of experience doing it.

And second, one of their own, Major Ricky J. Nussio, in a monograph titled "Tanks in the Street, Lessons Learned Through Bytes Not Blood," quotes a book about the war in Chechnya which offers the following stark image about an armored relief column: "According to the participants in the battle, a grenade launcher antitank shell then knocked out the column's command vehicle and the column lost any effective command. The tank immediately lit up like a torch...Each of the group's armored personnel carriers were pierced by at least five anttank grenades..."

So which will it be? The Next Generation U.S. Army? Or the Last Generation Russian Army?

By the way, if you want to reach an interesting account of Russian operations in Chechnya, which depended heavily on the use of wheeled personnel carriers with similar armaments like the Strykers', look at this Rand Corporation report: http://www.rand.org/publications/CF/CF162/CF162.appb.pdf . It contains some amazing details about Russian operational planning for the Russian's first invasion of Chechyna, including one where an entire Russian column was blocked from getting to Chechyna by a local automarket in Russia where some 8,000 people gathered regularly on Saturday's to buy and sell cars.

It's not really a laughing matter, of course. Presuambly, the Army knows the dangers of using even fast moving armored columns in hostile areas. For one they've just had a lot of experience doing it.

And second, one of their own, Major Ricky J. Nussio, in a monograph titled "Tanks in the Street, Lessons Learned Through Bytes Not Blood," quotes a book about the war in Chechnya which offers the following stark image about an armored relief column: "According to the participants in the battle, a grenade launcher antitank shell then knocked out the column's command vehicle and the column lost any effective command. The tank immediately lit up like a torch...Each of the group's armored personnel carriers were pierced by at least five anttank grenades..."

So which will it be? The Next Generation U.S. Army? Or the Last Generation Russian Army?

AND MANAGE TO LOCK IN THE FASTEST GROWTH IN PRICES 14 YEARS.

AND MANAGE TO LOCK IN THE FASTEST GROWTH IN PRICES 14 YEARS.

The best quote I've ever seen about how Europe could have fallen so head-long into madness is from F. Scott Fitzgerald's book, Tender is the Night.

"See that little stream--we could walk to it in two minutes. It took the British a month to walk to it--a whole empire walking very slowly, dying in front and pushing forward behind. And another empire walked very slowly backward a few inches a day, leaving the dead like a million bloody rugs. No Europeans will ever do that again in this generation."

"Why, they've only just quit over in Turkey," said Abe. "And in Morocco--"

"That's different. This Western Front business couldn't be done again, not for a long time. The young men think they could do it but they couldn't. They could fight the First Marne again but not this. This took religion and years of plenty and tremendous sureties and the exact relation that existed between the classes. The Russians and Italians weren't any good on this front. You had to have a whole-souled sentimental equipment going back further than you could remember. You had to remember Christmas, and postcards of the Crown Prince and his fianc�e, and little caf�s in Valence and beer gardens in Unter den Linden and weddings at the maire, and going to the Derby, and your grandfather's whiskers."

"General Grant invented this kind of battle at Petersburg in sixty-five."

"No, he didn't--he just invented mass butchery. This kind of battle was invented by Lewis Carroll and Jules Verne and whoever wrote 'Undine,' and country deacons bowling and marraines in Marseilles and girls seduced in the back lanes of W�rttemberg and Westphalia. Why, this was a love battle--there was a century of middle-class love spent here. This was the last love battle."

On the bright side, we had an excellent dinner at a restaurant called l'Apostrophe at 59, place Drouet d�Erlon in Rheims the night before. If you get to Rheims, a visit to the Cathedral there is worth your time. It's only an hour or so from Paris. And the stained glass windows behind the altar were done by Marc Chagall. A much nicer picture...

The best quote I've ever seen about how Europe could have fallen so head-long into madness is from F. Scott Fitzgerald's book, Tender is the Night.

"See that little stream--we could walk to it in two minutes. It took the British a month to walk to it--a whole empire walking very slowly, dying in front and pushing forward behind. And another empire walked very slowly backward a few inches a day, leaving the dead like a million bloody rugs. No Europeans will ever do that again in this generation."

"Why, they've only just quit over in Turkey," said Abe. "And in Morocco--"

"That's different. This Western Front business couldn't be done again, not for a long time. The young men think they could do it but they couldn't. They could fight the First Marne again but not this. This took religion and years of plenty and tremendous sureties and the exact relation that existed between the classes. The Russians and Italians weren't any good on this front. You had to have a whole-souled sentimental equipment going back further than you could remember. You had to remember Christmas, and postcards of the Crown Prince and his fianc�e, and little caf�s in Valence and beer gardens in Unter den Linden and weddings at the maire, and going to the Derby, and your grandfather's whiskers."

"General Grant invented this kind of battle at Petersburg in sixty-five."

"No, he didn't--he just invented mass butchery. This kind of battle was invented by Lewis Carroll and Jules Verne and whoever wrote 'Undine,' and country deacons bowling and marraines in Marseilles and girls seduced in the back lanes of W�rttemberg and Westphalia. Why, this was a love battle--there was a century of middle-class love spent here. This was the last love battle."

On the bright side, we had an excellent dinner at a restaurant called l'Apostrophe at 59, place Drouet d�Erlon in Rheims the night before. If you get to Rheims, a visit to the Cathedral there is worth your time. It's only an hour or so from Paris. And the stained glass windows behind the altar were done by Marc Chagall. A much nicer picture...

(The Eye of the Homeland, coming to a neighborhood near you...)

The military has promised us that the use of unmanned aerial vehicles in a "battlespace" gives friendly forces an unblinking eye with which to constantly survey events on the ground and gater intelligence.

Of course there's no reason that the same technology can't be hovering above U.S. airpace as well, is there? Well...the only reason is that the FAA, up until now, has been worried about dozens of UAVs in the air colliding with civillian aircraft that ARE manned, sometimes with hundreds of people.

But

(The Eye of the Homeland, coming to a neighborhood near you...)

The military has promised us that the use of unmanned aerial vehicles in a "battlespace" gives friendly forces an unblinking eye with which to constantly survey events on the ground and gater intelligence.

Of course there's no reason that the same technology can't be hovering above U.S. airpace as well, is there? Well...the only reason is that the FAA, up until now, has been worried about dozens of UAVs in the air colliding with civillian aircraft that ARE manned, sometimes with hundreds of people.

But

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}